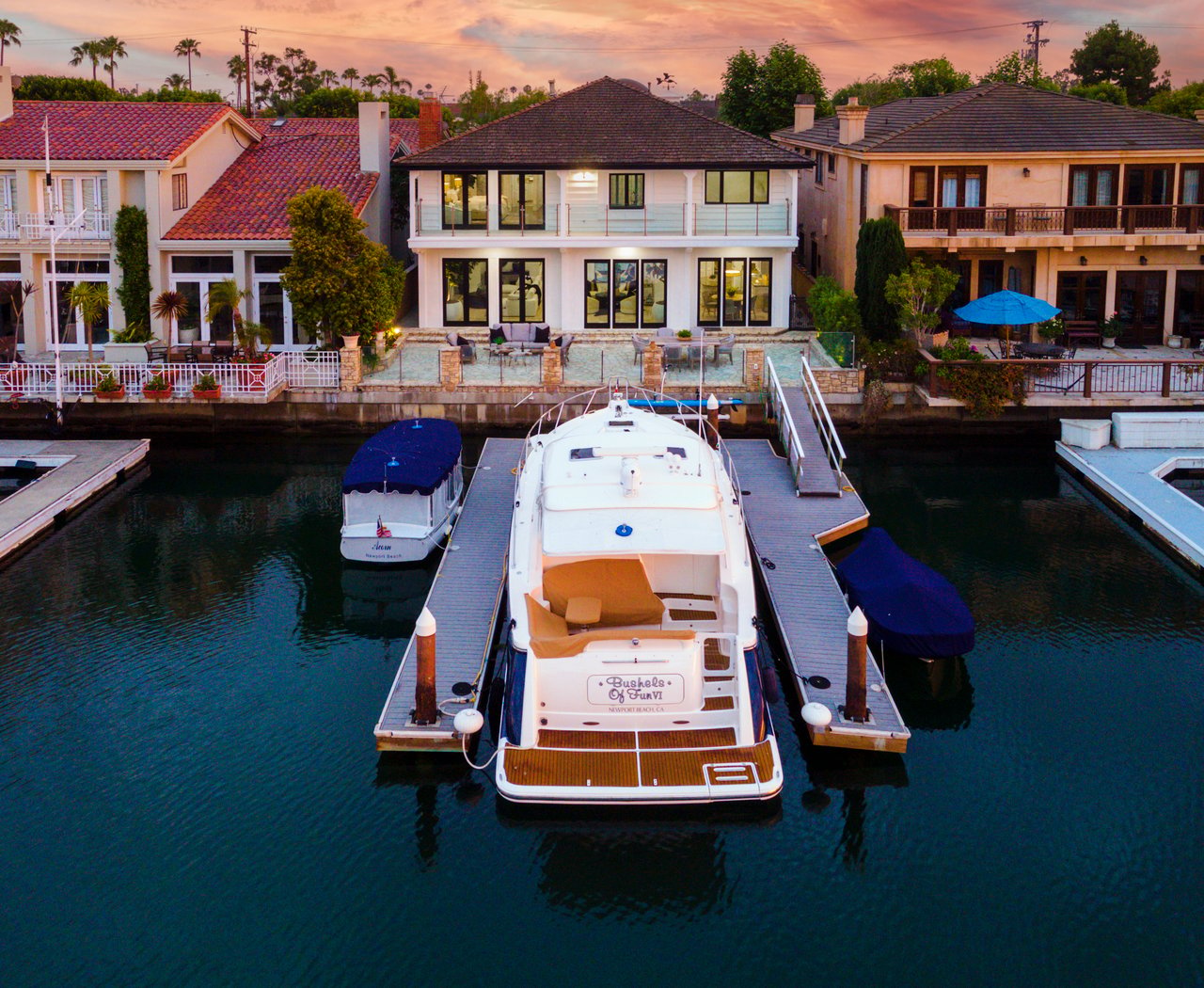

Why Luxury Buyers Walk Away During Escrow in Newport Beach and Coastal Orange County

Why do luxury buyers back out during escrow?

Luxury buyers most often walk away during escrow for one of five reasons: an inspection turns up something they didn't budget for, the appraisal comes in below the contract price, their financing falls through, their own home sale collapses, or their circumstances change for reasons that have nothing to do with the house. Nationally, Redfin reported that 13.7% of home purchase agreements canceled in January 2026, the highest January rate since it began tracking the data in 2017. In coastal Orange County, where nearly every transaction above $3M requires jumbo financing and escrows often run longer than the national average, sellers need to understand these risks before they accept an offer, not after.

We have personally sold more than 1,300 expired and cancelled listings over 35 years in this market. That number exists because deals fall apart, often for reasons that had nothing to do with the home itself and everything to do with how the offer was structured in the first place.

If you're preparing to list and want to understand what could derail a sale before it happens, here's what actually causes luxury buyers in Newport Beach, Laguna Beach, and Corona del Mar to walk.

The Most Common Reasons Luxury Buyers Walk Away

The inspection turns up something the buyer didn't price in. Older coastal homes, especially the original-stock cottages in Corona del Mar's Flower Streets or hillside properties in Laguna's canyons, often carry deferred maintenance that doesn't show up until a contractor opens a wall or crawls under the foundation. Galvanized plumbing, knob-and-tube wiring, drainage issues on a sloped lot, or a roof nearing the end of its life can shift a buyer's math by six figures overnight. I've written before about how to think through this decision before you ever list, including whether renovating before you sell makes sense for your situation.

The inspection turns up something the buyer didn't price in. Older coastal homes, especially the original-stock cottages in Corona del Mar's Flower Streets or hillside properties in Laguna's canyons, often carry deferred maintenance that doesn't show up until a contractor opens a wall or crawls under the foundation. Galvanized plumbing, knob-and-tube wiring, drainage issues on a sloped lot, or a roof nearing the end of its life can shift a buyer's math by six figures overnight. I've written before about how to think through this decision before you ever list, including whether renovating before you sell makes sense for your situation.

The appraisal comes in below the contract price. This is the single most common reason a luxury deal falls apart after both sides have already agreed on a number. Coastal Orange County's best properties don't trade on price per square foot. A bluff-top lot in Crystal Cove, a full white-water view in Irvine Cove, or a rebuilt estate on Lido Isle can sell well above what a comparable-sales appraisal supports, because the comps themselves are thin and inconsistent. I covered why this gap exists in more detail in why luxury pricing in Laguna Beachis more complex than price per square foot. When the appraisal lands low and the buyer's loan is sized to the appraised value, the buyer either has to bring more cash to the table or walk.

The buyer's financing falls through. Most purchases at this price point require financing that goes well above conforming loan limits. For buyers who are self-employed or whose income comes from investments, business ownership, or carried interest, lenders are asking for two to three years of tax returns and verifying liquidity down to the source. If that documentation doesn't hold up, or if a rate lock expires during a long escrow and the buyer's debt-to-income ratio no longer works at the new rate, financing dies quietly and the deal goes with it.

The buyer's own sale falls apart. A meaningful share of buyers at this price point are selling a home of their own to fund the purchase. If their buyer walks, or their escrow drags past the date they need cash in hand, the chain breaks. This is one of the reasons I always want to know, before we accept an offer, whether a buyer's purchase depends on a sale that hasn't closed yet.

Something changes that has nothing to do with the house. A job offer falls through. A divorce gets contentious. A buyer's spouse who hasn't seen the property in person finally flies out and says no. None of this is predictable, and none of it is something a seller can fully insure against. But it's also rarer than the first four reasons, and it's the one category where pricing, preparation, and contract structure can't help you.

Why Coastal Orange County Escrows Carry Extra Risk

A few things about this market make escrow more fragile here than in a typical suburban transaction.

Financing requirements are more rigorous. At these price points, every buyer's loan is underwritten on its own merits, and lenders typically ask for more documentation, verified income, and larger reserves than buyers may expect from previous purchases.

Longer marketing times mean more time for things to change. Right now, Corona del Mar has roughly two dozen homes in escrow that spent a median of around 70 days on the market before their buyer signed, based on the most recent MLS data I track. The longer a home sits, the more leverage a buyer can feel they have once they're under contract, and the more likely they are to use the inspection period to renegotiate rather than walk outright, though some do both. I broke down what days-on-market data actually signals about a property's negotiating position in what average days on market reveals about Corona del Mar's market strength.

Coastal-specific disclosures add complexity. Bluff-top and ocean-front properties in Laguna Beach and Corona del Mar can carry geologic, erosion, or Coastal Commission considerations that don't exist inland. Gated communities like Pelican Crest, Big Canyon, Three Arch Bay, and Emerald Bay come with HOA documents, CC&Rs, and sometimes architectural review requirements that a buyer's attorney will want time to review. Every one of these is a point where a buyer with cold feet can find a reason to pause, extend, or exit.

How Sellers Reduce the Odds of a Buyer Walking

Most of what causes a luxury escrow to collapse is visible before the home ever goes on the market, if you know where to look.

Get ahead of the inspection. A pre-listing inspection lets you address or disclose issues on your terms, not the buyer's. It also removes the single biggest source of last-minute renegotiation.

Price to what the home will appraise for, not just what it might sell for. A number that's defensible against comparable sales, with a clear explanation for any premium tied to view, lot position, or finish quality, holds up far better when the appraiser shows up.

Vet the buyer's financing before you accept, not after. A pre-approval letter is a starting point, not proof. I look at the lender, the loan type, the buyer's down payment source, and how long their rate lock runs relative to the proposed closing date before I advise a client on which offer to take, especially when the highest offer isn't always the strongest one.

Structure contingency periods deliberately. Shorter inspection and appraisal contingency windows reduce the amount of time a buyer has to find a reason to renegotiate, without being so aggressive that you scare off serious buyers.

Keep a backup plan in motion. Even a strong escrow benefits from a seller who hasn't gone dark on other interest. If a deal does fall apart, the homes that re-list quickly and confidently, rather than sitting in limbo, tend to recover faster.

If you're getting ready to list and want a strategy built around minimizing the risk of a buyer walking away during escrow, this is the kind of situation I walk clients through before problems show up, not after.

Call or text me at 949-677-5268 and we'll go through what to expect and how to prepare.

Frequently Asked Questions

What happens to the earnest money deposit if a luxury buyer walks away during escrow?

It depends on whether the buyer is acting within a contingency period that's still open. If the buyer cancels while a contingency, such as inspection, appraisal, or loan approval, is still active and properly documented, the deposit is typically returned to them. If the buyer cancels after removing those contingencies, the seller may be entitled to keep the deposit as liquidated damages, subject to the specific terms of the purchase agreement.

How common is it for luxury home sales to fall through?

More common than most sellers expect. Nationally, Redfin reported that roughly 1 in 7 home purchase agreements canceled in January 2026, the highest January figure on record. Luxury transactions carry additional risk because of jumbo financing requirements and the thinner pool of comparable sales used in appraisals.

Can a seller keep a backup offer ready in case a buyer walks?

Yes. Many sellers accept a backup offer that becomes active only if the primary escrow falls through. This doesn't replace the need to manage the primary escrow carefully, but it does shorten the gap if a deal does collapse.

What's the difference between an appraisal contingency and a financing contingency?

An appraisal contingency lets a buyer cancel or renegotiate if the home appraises below the contract price. A financing contingency lets a buyer cancel if they're unable to secure their loan, for reasons ranging from documentation issues to a change in their debt-to-income ratio. Both are common in high-value transactions and both can end an escrow if not addressed early.

How long does escrow typically take on a luxury coastal Orange County home?

Most escrows run 30 to 45 days, though jumbo financing, coastal disclosures, or HOA document review can extend that timeline. The longer an escrow runs, the more opportunities exist for a buyer's circumstances, financing, or confidence to change.